AI Portfolio Optimization in the Agentic Era: Redefining the Efficient Frontier

.png)

In 2026, AI-powered portfolio optimization moved beyond predictive analytics to become agent-based asset allocation. Unlike legacy machine learning, this cognitive approach delivers deterministic inference, maintaining alpha during unprecedented regime shifts.

Think of the market as a conversation - a vast, overlapping roar of whispers, screams, and sudden, eerie silences. For years, we’ve been told that the right “wrapper” or faster “predictive tool” can turn that noise into certainty. But during the volatility spikes of 2024-2025, these tools didn’t just fail, they froze.

The Mirror of Correlated Errors

We’ve seen it in every CIO’s eyes- the realization that their sophisticated “Optimization as a Service” was simply a recitation of a script from a world that no longer exists.

- The Echo Chamber: Public LLM wrappers began to hallucinate market correlations, mistaking the reflection of their own logic for the real signal.

- The Consensus Trap: As thousands of quantum measurements were connected to the same extraneous “black boxes,” the exit door became impossibly narrow as everyone tried to leave at the same time.

- The Fragile Shield: Static models built on the comfort of historical averages shattered the moment the market stopped acting like a textbook and started acting like a living, breathing entity.

Betrayal of the “Black Box”

True fiduciary duty cannot survive behind a veil of “probabilistic guesswork.” When an outdated model goes wrong, it fails to explain why, leaving the portfolio manager accountable for logic he never truly owned.

In those critical moments of 2025, it was not a lack of data that cost billions, but a lack of a Sovereign Cognitive Core capable of independent thought.

To meet the SEC’s 2026 fiduciary standards, the industry is abandoning “optimization as a service” in favor of an infrastructure that treats transparency as an inherent requirement, not a feature.

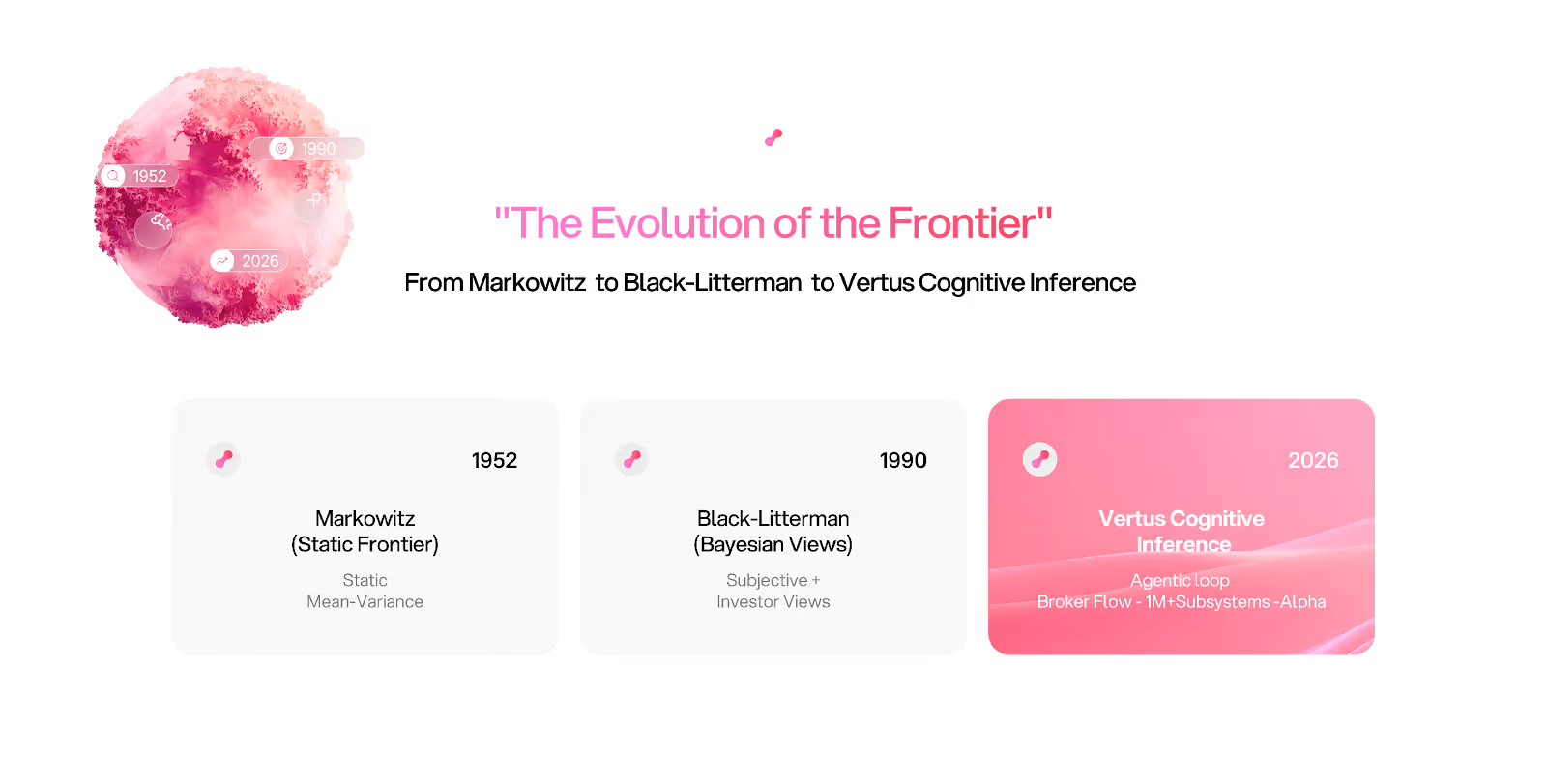

Beyond the Efficient Frontier: Adaptive AI for Capital Markets

The era of static models has reached its conclusion. In 2026, dominance in capital management belongs solely to those who adapt to the present faster than the market can react.

Markowitz’s traditional "Efficient Frontier" was architected for a linear world that no longer exists. Modern markets are complex systems defined by non-linear relationships, where standard diversification often transforms into a trap during correlation shocks.

Adaptive AI by Vertus abandons rigid forecasting in favor of continuous cognitive analysis. Instead of attempting to guess an asset's price a month in advance, the system focuses on the "market regime" here and now.

This allows a portfolio to evolve alongside the market landscape, maintaining resilience where traditional algorithms suffer terminal failure.

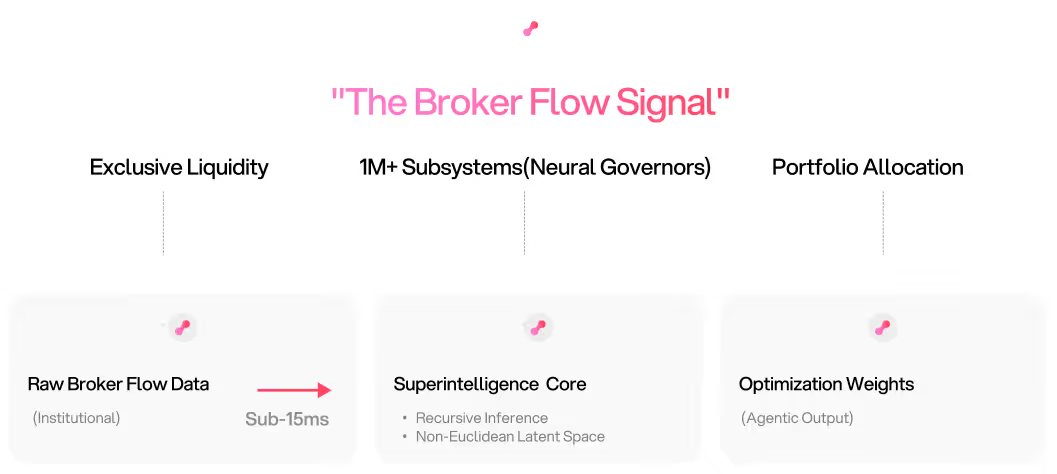

The Superintelligence Moat: How 1M+ Subsystems Create a "Self-Healing" Portfolio

At the core of our technology is the Superintelligence Core, an ecosystem comprising over 1,000,000 specialized subsystems. This is not merely a large neural network. It is a sophisticated fabric of "digital agents," each responsible for a distinct facet of market reality.

- Parallel Stress-Testing: As you read this sentence, the system simultaneously runs trillions of scenarios, identifying hidden liquidity risks before they manifest.

- Neural Governors: These subsystems act as internal regulators, automatically adjusting leverage and exposure upon detecting instability within the data's latent space.

- Self-Healing: If a specific strategy begins to degrade due to a regime shift, the architecture autonomously redistributes compute power to more relevant subsystems. This creates a portfolio "immunity" to market anomalies.

Non-Linear Market Reasoning: Why "Broker Money Flow" is the Critical Input for True Optimization in 2026

Most optimization systems from 2024 relied on public price charts and fundamental indicators - data that is already "priced in." Vertus moves beyond the visible spectrum.

In 2026, the primary fuel for alpha is Broker Money Flow (institutional capital movement). Our cognitive algorithm utilizes non-linear reasoning to analyze raw liquidity flows that have yet to appear on public charts.

- Hidden Liquidity Detection: Understanding where large-scale capital is accumulating allows the system to adjust portfolio weights before the mass price movement begins.

- Recursive Inference: The system constantly updates its "world model," integrating every new tick of money flow data back into the logic core. This ensures a Sub-15ms response to shifts in institutional sentiment.

Under the new SEC 2026 standards, cognitive adaptivity is moving from a competitive advantage to a fiduciary requirement for protecting investor interests during extreme market turbulence.

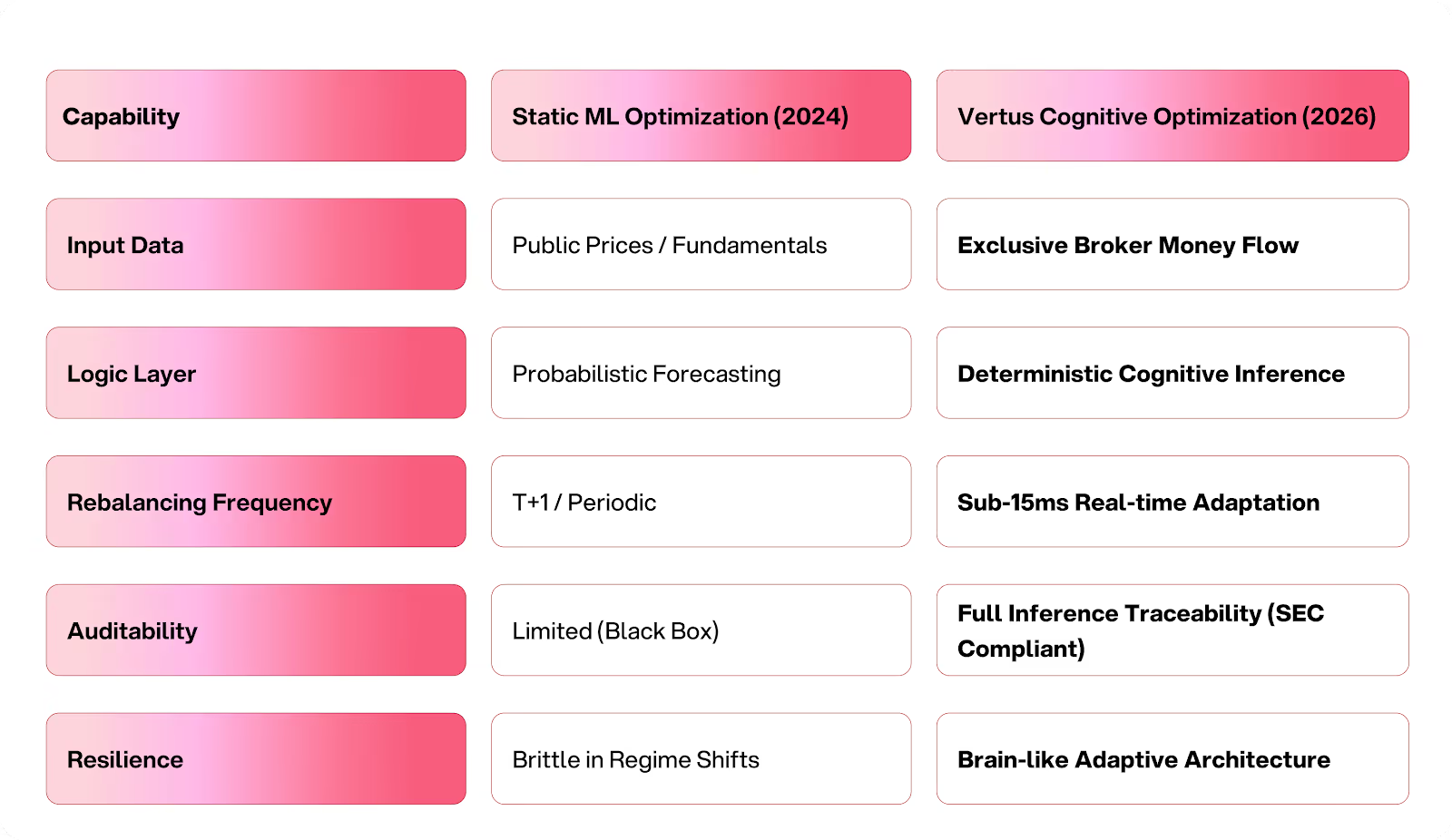

The Optimization Realignment: 2024 vs. 2026

The shift from predictive to agent-based logic represents a complete structural overhaul of how institutional portfolios are constructed. It is the difference between a system that simply guesses and a system that actually reasons.

The following comparison reflects the technical displacement of legacy probabilistic models by the Vertus deterministic cognitive architecture.

Infrastructure vs. Programmatic API

Scaling a cognitive strategy is more than just code. It is about owning a proprietary superintelligence core that breathes in unison with the market. Are you prepared to entrust your capital to a system that understands the very nature of every trade?

Vertus provides two pathways to this autonomy.

Vertus Institutional Infrastructure

For uncompromising resilience, our institutional hedgefund infrastructure creates a sovereign, air-gapped environment. Here, Zero Data Retention (ZDR) becomes your digital immunity, ensuring that not a single fragment of research ever leaves the walls of your fund.

The Intelligence API for Quant Researchers

Teams accustomed to forging their own success leverage the Intelligence API for Quant Researchers to stream cognitive signals into their existing OMS/EMS. This delivers <15ms Inference Latency, allowing for the deployment of agentic workflows at speeds the competition cannot reach.

To meet SEC 2026 Fiduciary Standards, the industry must leave the era of "AI Washing" behind. Real trust is built on infrastructure that ensures absolute traceability for every optimization decision.

Strategic FAQ

Q1: How does agentic AI optimize portfolios differently than standard algorithms?

A: Agentic AI uses "Recursive Inference," meaning it doesn't just follow a set of rules. It updates its worldview and allocation logic as new liquidity data enters the system.

Q2: What is the role of 1M+ subsystems in portfolio optimization?

A: They function as parallel "Neural Governors," stress-testing trillions of scenarios simultaneously to ensure the portfolio remains resilient against tail risks.

Q3: Is Vertus compatible with existing institutional OMS/EMS systems?

A: Yes, through our Intelligence API, firms can stream cognitive optimization signals directly into their existing execution stacks.

.avif)